Blogs

Investing should evolve with your age, income, and responsibilities. In your 20s, focus on building a strong foundation with higher equity exposure, early SIP investments, and an emergency fund. In your 30s, balance growth with stability by securing term insurance, planning for long-term goals, and increasing retirement contributions. In your 40s, shift toward wealth protection, reduce risk gradually, and prepare for retirement with structured planning. Each decade serves a purpose — build, grow, and protect. The key to financial freedom is starting early, staying consistent, and aligning investments with long-term goals.

Choosing between Mutual Funds and Fixed Deposits depends on your goals, risk tolerance, and time horizon. Fixed Deposits offer guaranteed returns and capital safety, making them suitable for conservative investors and short-term needs. Mutual Funds provide higher growth potential, better inflation-beating ability, and greater tax efficiency, but involve market risk. In 2026, smart investing is not about choosing one over the other blindly — it’s about using the right investment for the right purpose. A balanced strategy combining safety and growth can help build long-term wealth while maintaining financial stability.

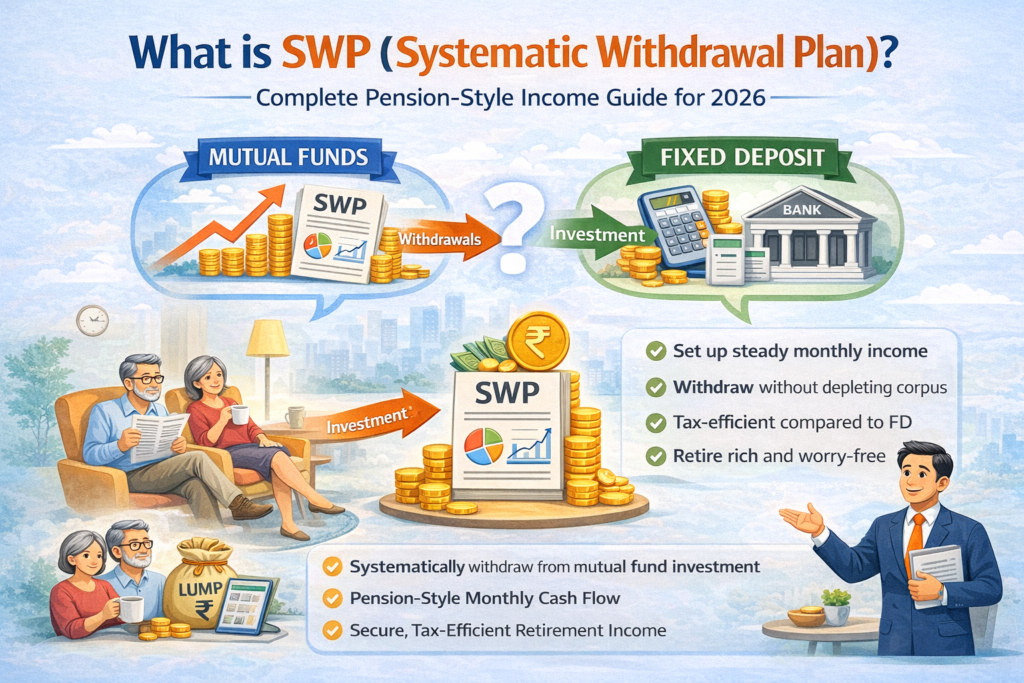

A Systematic Withdrawal Plan (SWP) allows you to withdraw a fixed amount regularly from your mutual fund investment while keeping the remaining money invested. It is an effective strategy for retirees or individuals seeking passive income. Unlike fixed deposits, SWP withdrawals are more tax-efficient because tax applies only to the capital gains portion, not the entire amount. With proper planning and a controlled withdrawal rate, SWP can help generate steady monthly income while managing inflation and preserving capital over the long term.

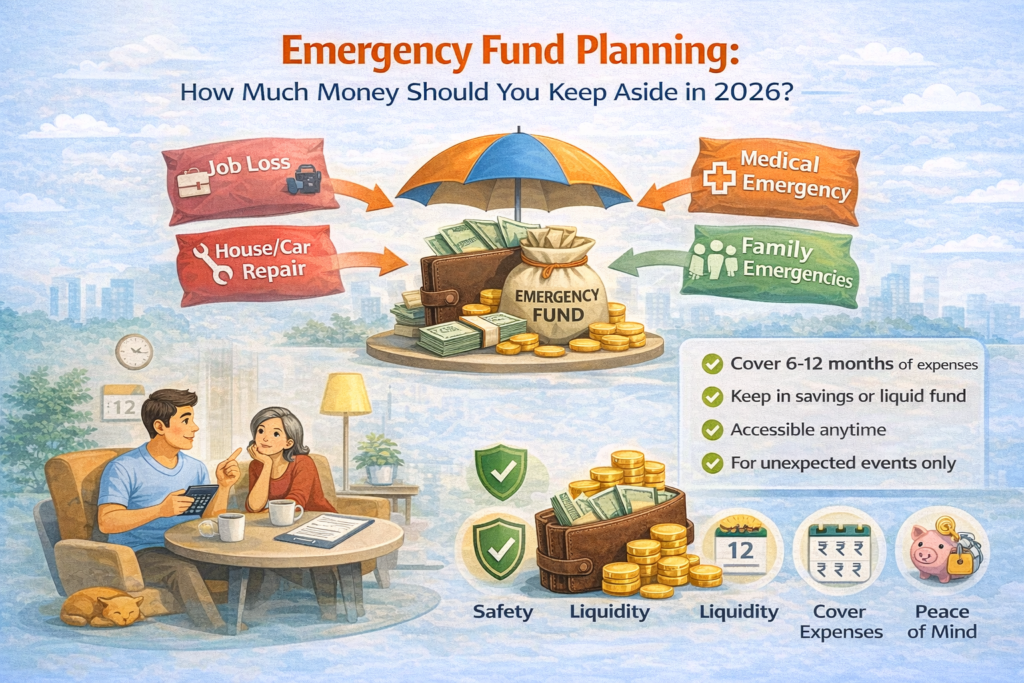

An emergency fund is the foundation of financial security. It protects you from unexpected situations like job loss, medical emergencies, business slowdowns, or urgent repairs. Ideally, salaried individuals should keep 3–6 months of expenses aside, while self-employed or single-income families should maintain 6–12 months of expenses. The goal is not high returns, but safety, liquidity, and quick access. Keep your emergency fund in a savings account or liquid fund, separate from daily spending. Building this safety cushion ensures peace of mind and prevents breaking long-term investments during crises.

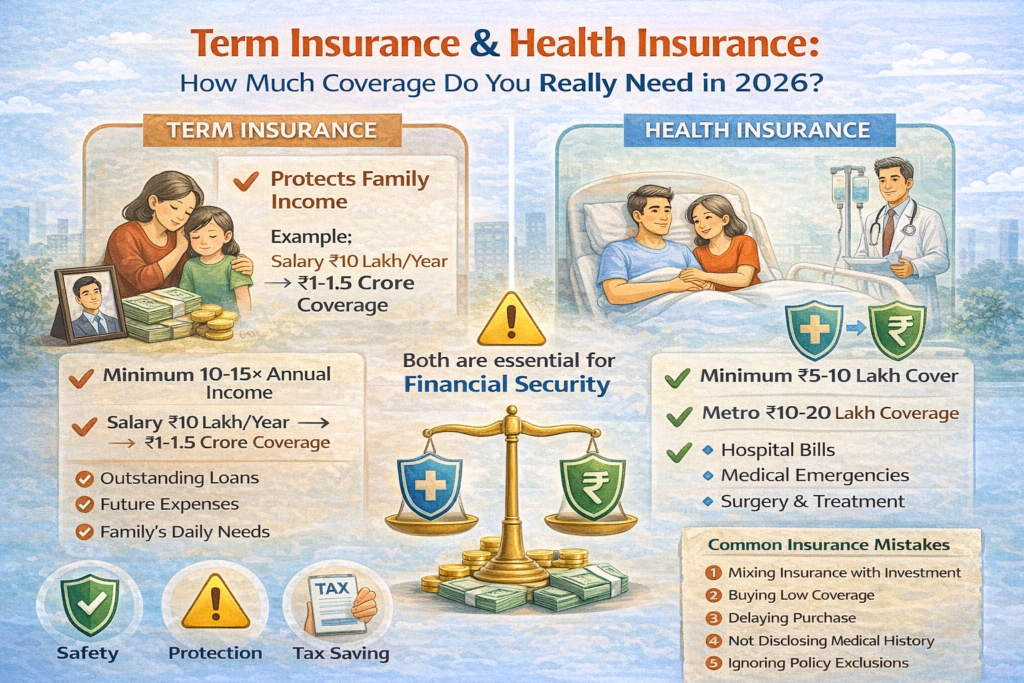

Insurance is the foundation of financial security. Term insurance protects your family’s future by replacing your income in case of an unfortunate event, while health insurance safeguards your savings from rising medical expenses. In 2026, experts recommend term coverage of at least 10–15 times your annual income and health insurance coverage of ₹5–10 lakh minimum, higher in metro cities. Without adequate protection, one emergency can disrupt years of financial planning. The right coverage ensures stability, peace of mind, and long-term financial resilience for your family.

Wealth creation is not about how much you earn, but how wisely you manage your salary. Whether you earn ₹25,000 or ₹1,00,000 per month, a structured budgeting approach can help you build long-term financial security. Following a disciplined rule like 50-30-20 — or adjusting it based on your income level — ensures proper allocation toward needs, lifestyle, and investments. Prioritizing emergency funds, insurance, and SIP investments can steadily grow your wealth over time. Consistency, controlled spending, and increasing investments with salary growth are the real keys to financial success.